The Perp DEX Wars - How Hyperliquid Ruled and Who’s Catching Up

Decentralized perpetual futures exchanges (“perp DEXs”) have exploded from a niche experiment into a trillion-dollar battleground. In early 2024, on-chain perpetuals averaged only a few billion dollars in daily trading. By the first week of October 2025, daily perp DEX volumes surged past $100 billion[1], even topping $1.05 trillion in a single month (Sept 2025). The milestone marked a 48% jump from the previous month, signaling that decentralized derivatives are no longer a backwater corner of DeFi - they’re now competing head-to-head with centralized venues.

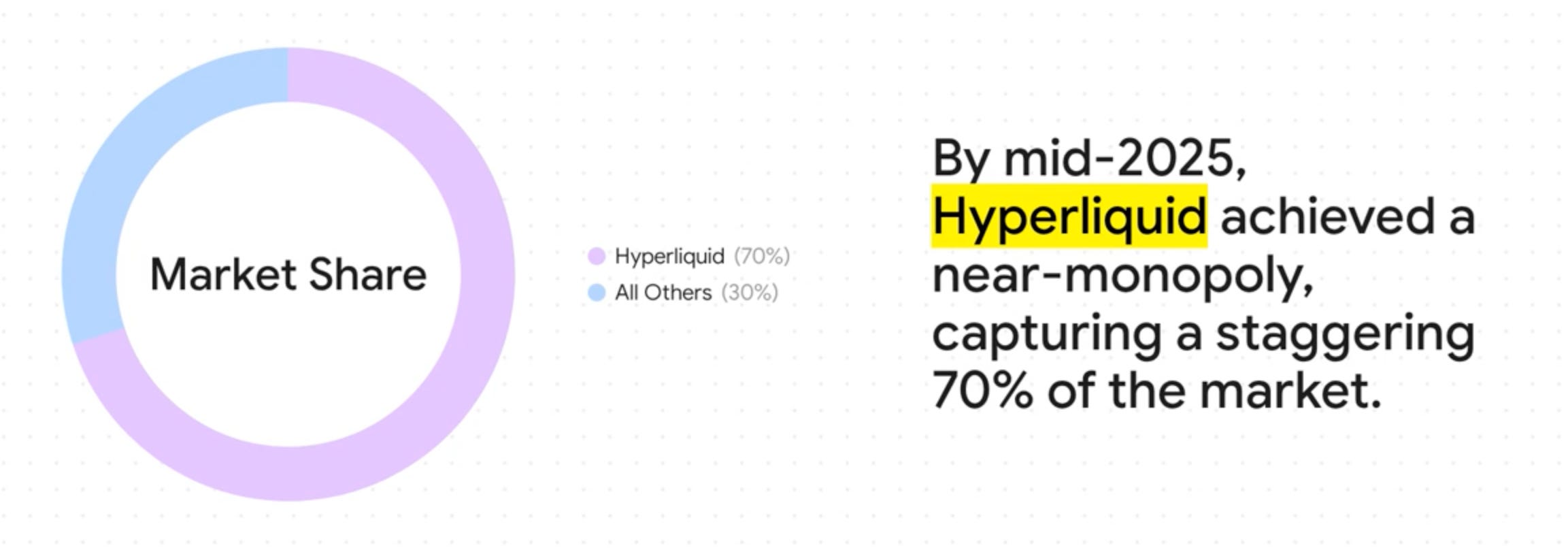

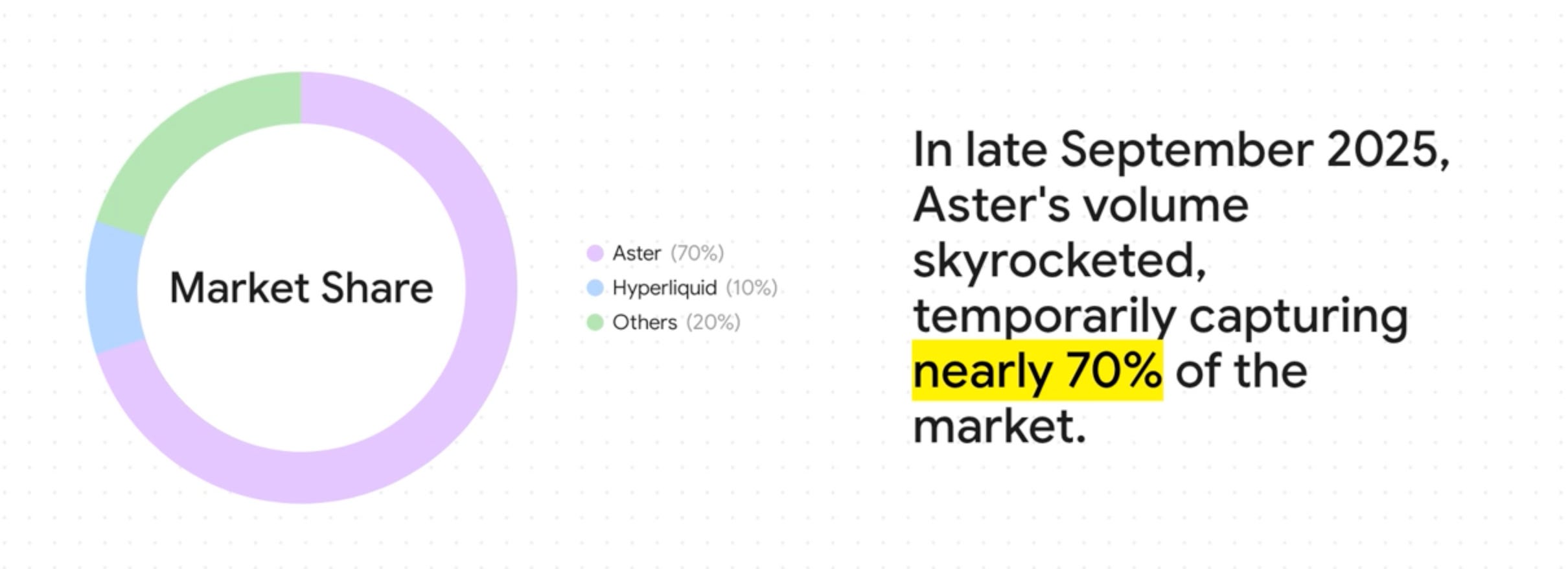

For much of the past year, Hyperliquid reigned supreme. This custom-chain perp DEX set a new performance benchmark and at one point captured ~70% of the market[2]. But as volumes boomed, challengers emerged. By October 2025, Hyperliquid’s dominance dramatically ebbed - slipping to barely ~10% share in late September, as aggressive upstarts like Aster and Lighter stormed onto the scene. What had been a one-DEX show turned into a three-way race. On some days, Aster’s trading volume even surpassed $36 billion in 24 hours, more than double the rest of the market combined, while Hyperliquid processed a “mere” ~$10B that day. Lighter, still in invite-only beta, quietly built to $7-8B daily volume by October. Suddenly, liquidity and traders were fragmenting across multiple platforms, each with its own innovations. The era of a single on-chain perp exchange monopoly was over.

This report dives deep into the ongoing Perp DEX Wars: how Hyperliquid achieved near-monopoly with a technical tour de force, why new entrants are challenging its throne, and what comes next. We’ll analyze the macro trends fueling on-chain derivatives, dissect past failures (dYdX, GMX, Mango) that paved the way for today’s contenders, and then explore each major player - Hyperliquid, Aster, Lighter - from matching engine architecture to risk models, latency, and token economics. We’ll see how Hyperliquid’s early lead is being attacked by Aster’s multi-chain blitz and Lighter’s zero-fee zk-rollup approach. We’ll examine “pop markets” like memecoin frenzy and stock perps that stress-test these exchanges’ depth and risk controls. Then, we’ll dig into the financials: volumes, open interest, fees, and revenue. Short equations will illustrate concepts like funding rate mechanics and price impact on depth. Finally, we’ll sketch scenarios for how this war could play out - and the broader implications for traders and investors. Let’s dive in, because the first true perp DEX battle in crypto history is underway1, and the stakes (and volumes) have never been higher.

Macro: From Zero to Trillions - The Perfect Storm for Perps

Not long ago, decentralized derivatives were an aspirational idea. In 2022, decentralized exchanges for perpetual futures barely scratched the surface of what centralized giants (Binance, OKX, etc.) were doing. But by 2025, all the pieces fell into place for a paradigm shift in trading infrastructure. The data is striking: between 2023 and 2025, annual perp DEX volume jumped from under a trillion to over $1.5 trillion, a >100% year-on-year surge[3]. September 2025 alone saw $1.05T traded on decentralized perps - roughly 10-15% of the total crypto futures market, up from low single-digits just a year prior. In other words, on-chain venues are finally chipping away at what was long a fortress of centralized exchanges.

What changed? Several macro drivers converged:

Post-FTX Trust Shift: The collapse of major CeFi platforms (like FTX in late 2022) left many traders scarred by custody and transparency risks. This psychological overhang primed the community to seriously consider non-custodial alternatives where “code is law” and users hold their own keys. Perp DEXs, once seen as clunky and illiquid, suddenly became attractive as a safer harbor for serious traders, provided they could perform. The on-chain derivatives space had a clear opening if someone could deliver CEX-like experience without the counterparty risk.

Maturing Infrastructure: By 2024-25, the underlying blockchain tech caught up to the demands of high-speed trading. Faster execution layers, cheaper transaction costs, and reliable oracle feeds enabled on-chain trades at speeds that were unthinkable a few years prior4. Specialized app-chains and Layer-2 rollups emerged, purpose-built for low-latency trading. In short, the old excuses (“too slow, too expensive”) started to melt away as innovative developers optimized every layer of the stack.

Proof of Concept - Hyperliquid’s Breakthrough: Crucially, Hyperliquid’s success proved a point: a DEX can scale to centralized exchange throughput and beyond2. Hyperliquid’s appchain achieved sub-second finality and massive throughput, demonstrating that if you engineer for speed and bootstrap liquidity cleverly, traders will come. This proof-of-scale was a wake-up call - it “unlocked venture appetite in a way we didn’t see last cycle,” as one investor put it. Once Hyperliquid hit a critical mass of users and volume (billions per day) without blowing up, it de-risked the whole concept of on-chain perps for both traders and backers.

Venture Capital & “War Chests”: Where early DeFi derivatives were bootstrapped by communities, the big money started flooding in by 2025. Venture capital, freshly refocused on revenue-generating protocols, saw perp DEXs as potential cash machines - arguably among the most profitable business models in crypto[5]. Investors who once chased fleeting DeFi fads rotated into funding the next Hyperliquid. “Most VCs have just caught on to how massive the pot of gold at the end of the perp DEX rainbow can be,” noted one VC, who predicted the winner here could become crypto’s first trillion-dollar company. Indeed, term sheets multiplied; at one point, “a couple of new perp DEXs a week” were pitching for funds. Projects like Bulk raised multi-million dollar seeds to join the fight. This influx of capital armed new entrants with incentive budgets and development resources - effectively war chests to spend on liquidity mining, marketing, and technical R&D. Wars are expensive, but deep pockets were now willing to spend in order to “win the war” (as we’ll see Hyperliquid and others explicitly doing).

User Base Rotation: On the demand side, a rotation occurred among traders and “degens.” The hot money that chased memecoins and prediction markets in early 2023 started shifting to perps by 2024 as those other manias cooled[1]. Perpetual futures have always been one of crypto’s highest-volume products (even on CEXs), so it was perhaps natural that speculative capital would eventually gravitate on-chain once the venues were viable. By 2025, on-chain perps offered not just crypto assets but equities, indexes, and more, giving a wide surface area for speculation. Combine that with token incentive programs (trading rewards, airdrop farming) and it’s easy to see why trading activity flooded into these platforms.

CEX Clamps and Global Access: Meanwhile, regulators were tightening screws on centralized derivatives (stricter KYC, leverage limits in some jurisdictions). Perp DEXs, being globally accessible and pseudonymous by nature, became a pressure release valve for traders facing offboarding or restrictions elsewhere. Want 50x leverage on a memecoin at 3 am on a Sunday? A few clicks on a DEX (with just a wallet) can get you that, no questions asked. This regulatory arbitrage fueled usage, though it also puts a question mark over how long the high-leverage, no-KYC model can persist (we’ll revisit this risk in the Scenarios section).

All these factors created a perfect tailwind for perp DEXs. By late 2024, decentralized futures were finally taking a non-trivial share of the total crypto derivatives pie. The Block’s data showed spot DEXs had slowly eroded centralized exchange share over years, but derivatives had remained a CEX stronghold - until now. In 2025, the inroads became undeniable. DeFi perps went from capturing ~5% of perp volume to around 10%+ of the market, and rising fast, as huge incentive programs and technical breakthroughs lured volume on-chain.

Crucially, it isn’t a winner-take-all story (yet). Instead, we have a full-blown arms race among a new breed of perp DEX platforms. Each is trying to outdo the others on speed, liquidity, features, and token rewards. As Jeff Dorman of Arca noted, “people spend money to win wars” - and indeed a rising tide may lift all boats in this sector, at least for now. Traders, mercenary or not, are being courted with ever-tightening spreads, lower fees, and higher incentives. The question everyone’s asking is: who will capture the lion’s share of this on-chain derivatives boom?

Before we analyze the top contenders, it’s worth looking back. The current war was enabled in part by the lessons (and failures) of earlier perp DEX attempts. From dYdX’s early dominance and controversial tokenomics to the fall of Mango Markets, previous generations charted the pitfalls to avoid. Understanding those failures will help explain how Hyperliquid managed to succeed - and why the new challengers have adopted very different strategies.

Failures and False Starts: Lessons from dYdX, GMX, Mango & More

Every revolution has its pioneers - and its casualties. The on-chain perps space is no different. Long before Hyperliquid or Aster, platforms like dYdX, GMX, Perpetual Protocol, Mango Markets, and others experimented with bringing perpetual futures to DeFi. Each contributed something (technically or conceptually), but none truly cracked the code to dethrone centralized futures at the time. By examining what went wrong for these early movers, we can appreciate how the current crop improved on their designs.

dYdX (V3 and V4) - The Cautionary Tale of Token Misalignment: Launched in 2020, dYdX was a trailblazer - an orderbook-style perp DEX that by mid-2021 had grown to dominate decentralized derivatives. At one point, dYdX accounted for over 66% of decentralized futures volume, effectively being the marquee name in the sector. It proved that with off-chain matching (StarkEx L2) and liquidity mining, you could attract serious volume. However, dYdX’s early success plateaued and then faltered in 2022-2023. Why? In hindsight, architectural and token-economic decisions undermined its long-term trajectory. dYdX’s V3 relied on a semi-centralized orderbook (off-chain order matching and a centralized price oracle) - it was fast, but not fully decentralized, and constrained by StarkEx throughput and Ethereum finality. More critically, dYdX launched a token ($DYDX) that, aside from governance and liquidity mining rewards, had no direct fee accrual to holders. The team and investors kept a large allocation, and the protocol’s trading fees largely went to an insurance fund or the treasury, not to token holders. This led to a lack of tokenholder alignment: traders farmed and dumped rewards, and long-term investors saw little fundamental value. As Arca’s analysis put it, a big part of dYdX’s flop was self-inflicted - they catered to VC profits over community value, and failed to evolve the product (limited markets, only ~20× leverage, etc.) to keep up. By the time dYdX tried a do-over with a Cosmos-based v4 (to fully decentralize), they had lost momentum. Liquidity mining ended, users had drifted to alternatives, and the new chain’s uptake was modest. dYdX went from first place to effectively “sidelined from the top ring of perp-DEX brawlers.” The lesson? Speed alone wasn’t enough - you also needed to share the economics or deeply integrate the token into the experience to retain loyalty. Hyperliquid would later seize on this insight by heavily aligning its token with platform revenue, as we’ll see.

GMX - Innovative Model, But Depth Constraints: While dYdX used a central limit order book, GMX (launched 2021 on Arbitrum & Avalanche) pioneered an AMM-like approach to perps. Traders could long or short assets against a pooled counterparty (the GLP liquidity pool), with prices fed by oracles. This virtual AMM model offered simplicity (no active market-makers needed) and strong token incentives: GMX’s token stakers earned real trading fees, a form of “real yield” that became popular. GMX achieved significant usage, especially after centralized exchange upheavals - at times GLP’s TVL swelled and GMX volumes rivaled smaller CEXs. However, as volumes scaled, GMX revealed inherent limitations: the pooled liquidity meant large trades could cause big slippage and shallow depth on volatile assets (especially long tail coins). Unlike an order book, where liquidity scales with maker participation, GMX’s pool had finite depth determined by GLP size and composition. This led to wider spreads and execution slippage for size, an issue professional traders balk at. Moreover, the GLP model introduced risk asymmetry - liquidity providers effectively take the other side of traders, profiting when traders lose and vice-versa. Big trader profits (e.g. on trending longs) could drain the pool. The design requires careful risk parameters and typically offers less leverage (e.g. 20-30× max). In summary, GMX proved that a decentralized perp could deliver a smooth UX and real fee revenue, but its AMM architecture struggled with liquidity for high-volume trading. It couldn’t match the orderbook model’s precision in price discovery, especially as on-chain volumes reached tens of billions. Many subsequent DEXs (including Hyperliquid, Aster) opted for CLOB designs to get tighter spreads and scalable depth[2].

Mango Markets - Risk Management Failure: Solana’s Mango Markets offered a high-performance orderbook DEX with cross-margin perps, and it gained some popularity in 2021-22. But Mango became famous for the wrong reasons: an October 2022 incident in which a rogue trader manipulated Mango’s thinly traded governance token price to borrow and drain over $116 million from the protocol6. The attacker essentially engineered an oracle exploit - using two accounts to pump MNGO token’s price nearly 40× in minutes, which boosted the value of collateral and let them borrow most of Mango’s liquidity, leaving the platform insolvent. This incident highlighted a key pitfall of on-chain perps: oracle and market manipulation risk. Mango’s risk controls and liquidity were insufficient to prevent a large actor from cornering the market. The aftermath was ugly (Mango depositors lost funds, though the attacker negotiated a partial return). The hack underscored that “fully transparent markets” can be exploited if not paired with robust safeguards. Any DEX relying on an illiquid token as collateral or loosely guarded price feeds is vulnerable. Hyperliquid’s team took note - later implementing things like dynamic risk limits and anti-manipulation rules after experiencing a smaller-scale incident on their platform (more on that in Pop Markets section). For the industry, Mango’s demise served as a cautionary tale that smart contract security and risk management are as critical as matching-engine speed. A flashy UI and fast chain mean little if a clever attack can bankrupt the exchange overnight.

Others - Perpetual Protocol, Serum, etc.: There were other notable attempts: Perpetual Protocol (formerly Strike), which used a virtual AMM (vAMM) model on xDai then Optimism, gained traction in DeFi summer 2021. But its initial design had issues with constant funding payments and “virtual” liquidity that made it hard to sustain deep markets. It pivoted to a Uniswap v3-based model (Perp v2) later, but by then newer entrants had leapfrogged it. Serum on Solana offered an on-chain orderbook (heavily used by centralized market makers), but it mainly supported spot; derivatives on Solana ended up on Mango/Drift. Drift Protocol on Solana did build a notable perp DEX with an innovative risk engine (dynamic pricing), but Solana’s turbulent 2022 (network halts, liquidity exits after FTX - which was a big Solana backer) stunted its growth. Injective launched its own chain for derivatives and orderbooks, but for a long time it saw modest volumes, partly due to limited ecosystem traction. Many early projects also suffered from being too early: the user base for on-chain perps was simply not large or willing to migrate until a post-2022 trust erosion occurred and until performance caught up.

Key Lessons: In sum, the first generation taught the importance of speed + depth + alignment. You need a performant engine (dYdX had that), but also deep liquidity and risk controls (dYdX’s semi-centralized model and GMX’s AMM both fell short here in different ways) and a token model that rewards users (dYdX failed there, GMX succeeded somewhat). The holy grail is to achieve CEX-like execution and DeFi-like community ownership. Hyperliquid’s brilliance was arguably in hitting that trifecta in 2024. It wasn’t burdened by VC extractive economics or slow general-purpose chains. Now, the challengers like Aster and Lighter are each trying to excel on different aspects - Aster on broad accessibility and aggressive incentives, Lighter on fairness and fee elimination - while learning from the past. And unlike early projects that had the field to themselves, these new competitors are directly battling a dominant incumbent (Hyperliquid) in a very high-stakes, high-volume environment. It truly is a war - and Hyperliquid’s near-monopoly in 2024 is now being stress-tested.

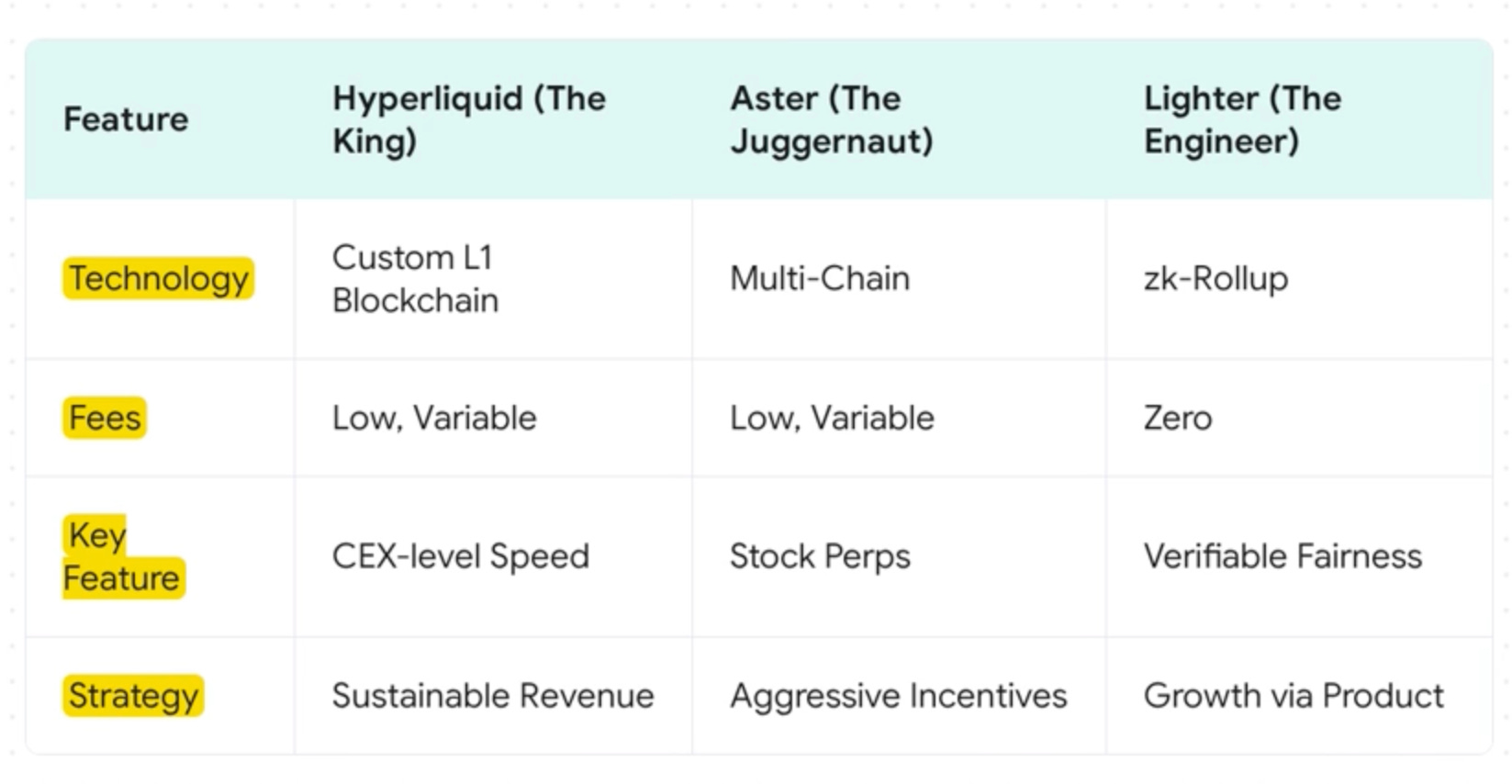

Hyperliquid: The On-Chain CEX - Architecture, Performance, and Monopoly Status

When Hyperliquid burst onto the scene in late 2023/early 2024, it felt like a cheat code for DeFi. Here was a DEX that traded like a centralized exchange - blazing fast, deep order books, minimal fees - yet it was fully on-chain and non-custodial. Hyperliquid’s achievement was to convince even hardened high-frequency traders that a decentralized platform could meet their demands. Let’s break down how Hyperliquid built its empire: from technical architecture to liquidity strategy to tokenomics. It’s essential to understand this, because Hyperliquid set the bar that all challengers are now measured against.

Custom Layer-1 “HyperChain” & Matching Engine: Hyperliquid wasn’t just an app on Ethereum or Solana - it’s an entire bespoke Layer-1 blockchain built for one purpose: speed[7]. The team recognized that general-purpose chains (even fast ones) introduced latency and throughput limits incompatible with a top-tier trading experience. As one investor quipped, “When your product is speed, you can’t have a slow foundation”. So Hyperliquid developed HyperCore, a custom consensus and execution engine optimized for a central limit order book (CLOB). Its consensus protocol, dubbed HyperBFT, achieves sub-200ms block finality and can process up to 200,000 orders per second - numbers that rival Nasdaq or Binance matching engines. This is not theoretical: in live conditions Hyperliquid routinely handles bursts of tens of thousands of TPS without lags. There are zero gas fees for trading on Hyperliquid (fees are abstracted to simple trading fees), eliminating the UX friction of gas calculation. The order book lives fully on-chain (every bid/ask and trade is a transaction, validated by HyperBFT validators), yet the user experience feels as smooth as using a centralized exchange web socket. By owning the entire stack (consensus + trading engine), Hyperliquid can finely tune performance - for example, validator nodes are highly optimized, and block propagation is designed around the order book message flow. This vertical integration (owning chain + exchange) follows the insight that “the path to L1 success is to own the chain, the DEX, and even the stablecoin”. Hyperliquid hasn’t launched a native stablecoin yet, but its architecture gave it a clear advantage in raw speed and reliability out of the gate.

Deep Liquidity via Innovative Market Making (HLP Vault): Speed alone doesn’t guarantee liquidity - you need market makers populating the order book with thick bid/ask walls. Hyperliquid tackled this through a novel community-driven liquidity program. It introduced the Hyperliquidity Provider (HLP) Vault, a pool where users can deposit assets to backstop market making. Essentially, users became passive liquidity providers to the order book, earning yields from market making profits and trading fees. Professional market makers (some likely internal or partners) use the HLP pool to quote two-sided markets on all trading pairs, meaning even newly listed assets start with decent depth. This hybrid approach combines the advantages of an order book (precision pricing) with an AMM-like pooled liquidity concept. The results have been impressive: Hyperliquid achieved tight spreads often on par with major centralized exchanges, and its peak total liquidity (sum of bids and asks) exceeded $500 million on the order books. The HLP vault delivered a steady ~6-8% APY to providers, making it attractive relative to passive DeFi yields. This incentivized more liquidity to join, reinforcing a virtuous cycle:

more liquidity → better execution → more volume → more fees for LPs.

In effect, Hyperliquid created institutional-grade depth on-chain. Large traders notice this - for example, you could fill a multi-million-dollar order for BTC or ETH perp on Hyperliquid with negligible slippage, a feat previously limited to CeFi venues. By consciously avoiding AMMs and instead going with a full CLOB, Hyperliquid unlocked superior price discovery and minimal funding rate dislocations. It’s the only DEX at the time that truly felt like trading on a Binance-level order book, which became a huge pull factor for serious traders.

Risk Management and Reliability: Running an on-chain exchange at this scale required Hyperliquid to also innovate on risk controls. Early on, they faced a stress event - a huge whale position on an illiquid token (XPL) that caused a major loss and forced liquidations. Rather than crumble, Hyperliquid responded by upgrading its risk engine: introducing dynamic margin requirements (higher margin for larger or riskier positions), price manipulation guards, and circuit breaker-like “stress alerts” for abnormal market moves. These measures paid off in mid-2025 when a meme coin called PUMP skyrocketed over 150%, putting one Hyperliquid trader’s $85.6B token short in a $35M unrealized loss - a potentially destabilizing situation[7]. Thanks to risk limits and active management, the position was not allowed to nuke the exchange; Hyperliquid contained the fallout (the trader’s account remained solvent with enough collateral, albeit hurting). The event did underscore how volatile “pop markets” can stress a DEX, but Hyperliquid’s swift adaptations (like raising margin on PUMP futures and using its insurance fund if needed) maintained platform integrity. These robust risk controls, combined with transparent, on-chain auditability, have given Hyperliquid a reputation for resilience. It’s notable that while centralized platforms occasionally suffer auto-deleveraging or clawbacks in extreme events, Hyperliquid so far has not imposed losses on its users beyond the at-fault accounts - a sign of prudent risk frameworks.

Token Economics - Community-Owned Liquidity Superpower: If Hyperliquid’s tech is CEX-like, its token economic model is pure DeFi genius. The platform’s native token HYPE was distributed with a community-first ethos: no VC allocations, large airdrops to early adopters (the team retroactively rewarded traders with HYPE on Nov 29, 2024, creating goodwill), and ongoing trading rewards. But the real kicker is how Hyperliquid uses its revenue. The exchange generates substantial fees - as of 2025, around $3-5 million per day in trading fees, putting it on track for $1+ billion in annualized revenue. Instead of pocketing these fees as profit, Hyperliquid directs the majority of fees to market buybacks of HYPE tokens on the open market. Over 2025, more than $715 million worth of HYPE was bought back and effectively burned or redistributed. This creates a powerful deflationary pressure on the token - as volume rises, more fees go into buybacks, shrinking supply and potentially boosting price. In essence, traders who use Hyperliquid are indirectly returning value to HYPE holders (which many traders also are, due to airdrops or purchases). This aligns incentives beautifully: users want to hold HYPE because the more they and others trade, the more value accrues to the token. It’s a feedback loop that dYdX notably lacked. The effect has been a strong token performance - by Oct 2025, HYPE was trading around ~$50 with a fully diluted market cap near $50 billion, reflecting the market’s belief in Hyperliquid’s cash flows and longevity. Unlike many exchange tokens, HYPE isn’t just a speculative promise; it’s directly tied to one of the highest revenue protocols in crypto. And crucially, because Hyperliquid did not sell large chunks of tokens to VCs at seed prices (it funded development via grants or small raises), there’s less sell pressure from insiders. The token distribution and revenue model have engendered deep user loyalty - traders feel they own a piece of the exchange’s success, and indeed they do.

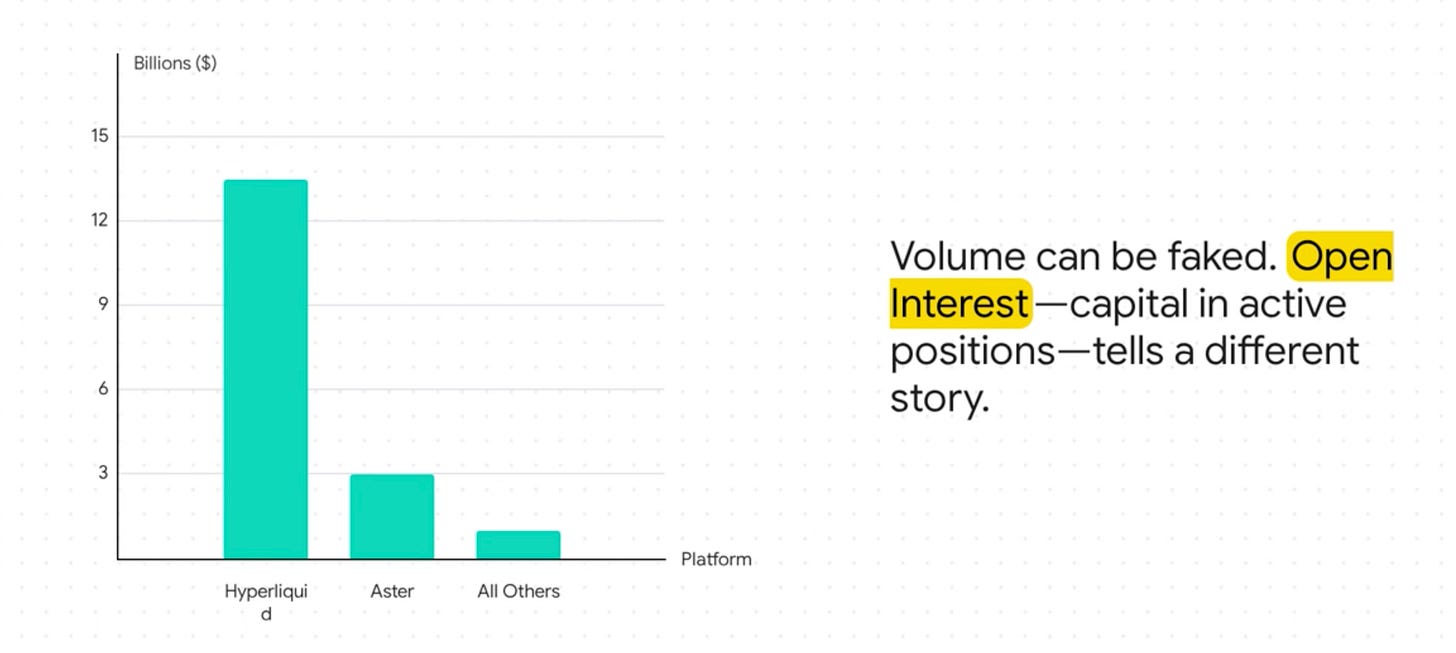

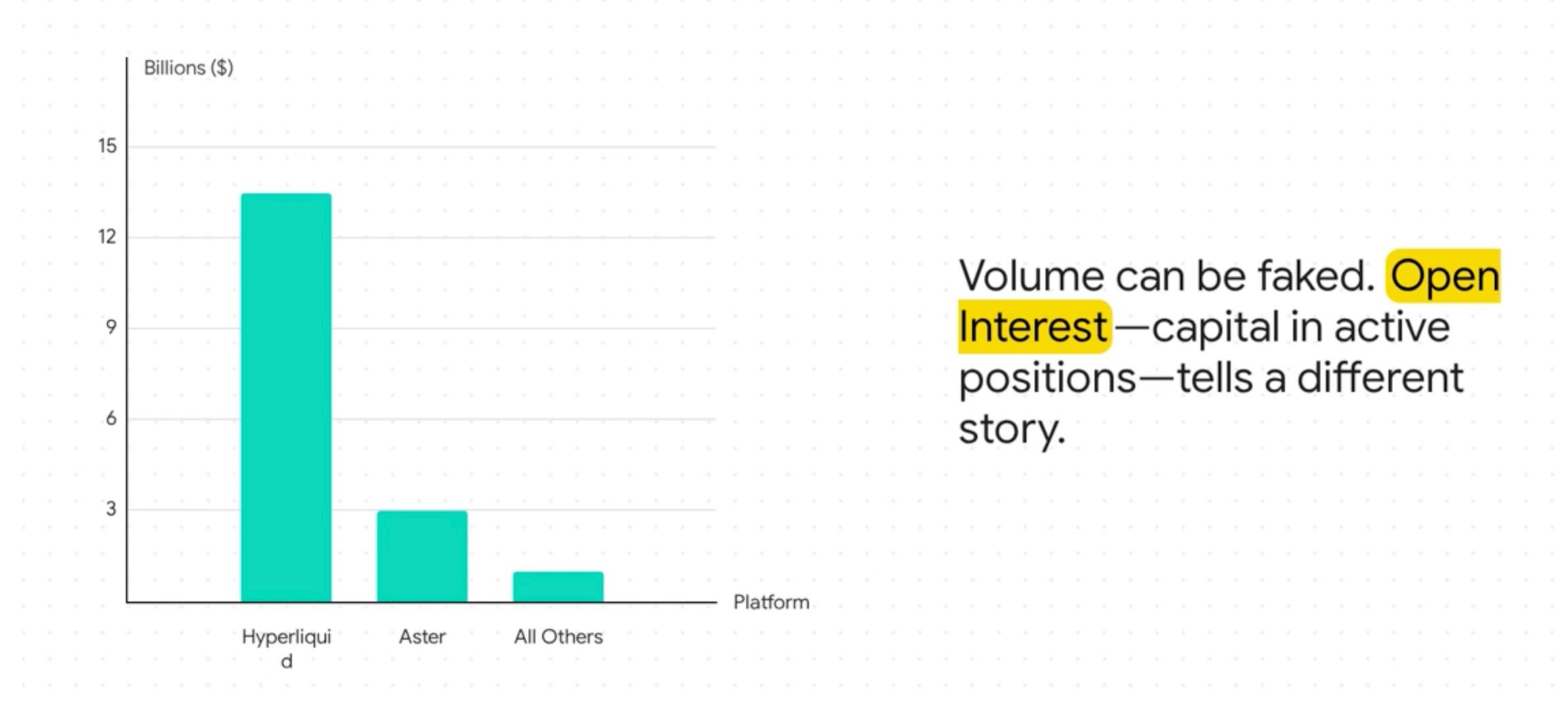

Monopoly Status - By the Numbers: By mid-2025, Hyperliquid’s strategy yielded astounding metrics. It consistently handled $10-15 billion in daily volume across a wide array of markets (BTC, ETH, majors, but also altcoins and even pre-launch tokens). Its open interest - a key indicator of how much capital is parked in positions on the exchange - hovered around $12-14 billion, dwarfing any other DEX’s OI by an order of magnitude. (For context, the second-largest OI on a DEX was under $1B; no one else was even close.) Hyperliquid had over 100 trading pairs, including exotic offerings like pre-IPO futures (e.g., it ran a market for the XPL token before it officially launched, allowing price discovery ahead of time). Its fee revenue in the 30 days up to Oct 8 exceeded $90 million, more than the entire DeFi protocol category in some prior months. By most measures, Hyperliquid looked like the winner - a decentralized exchange with centralized exchange performance and better tokenomics. Little wonder investors and analysts crowned it “the only DEX that fully replicates a CEX’s speed and reliability on-chain.”

However, success invites competition. Hyperliquid’s near-monopoly through early 2025 did not go unnoticed. Ambitious teams and big backers saw an opening: if Hyperliquid could build a hyper-fast appchain and capture billions in value, maybe someone else could do it differently - or convince traders to jump ship with even juicier incentives. By mid-to-late 2025, Hyperliquid’s “king of the hill” position started to be tested. It was still the king, especially in terms of open interest and loyal user base, but, as one commentator put it, “that buffer is thinning.”2 Hyperliquid now faces the classic dilemma of a pioneer: can it maintain its lead when deep-pocketed rivals are gunning for it with alternative offerings? In the next section, we’ll examine these challengers - who they are, what they’re doing differently, and whether they stand a chance at catching up to Hyperliquid’s formidable lead.

The Challengers: Aster, Lighter & the New Wave of Perp DEXs

Hyperliquid’s dominance hasn’t gone unchallenged. In 2025, a new cohort of perp DEXs emerged, each bringing a unique playbook to the battle. The two grabbing the most headlines are Aster and Lighter, but they are flanked by several other contenders like edgeX, Bulk, Drift, Pacifica, Zeta and more8. Let’s dive into the major challengers, focusing primarily on Aster and Lighter, which have in a short time seized significant volume. We’ll explore how their architectures and strategies differ from Hyperliquid’s - and the strengths (and weaknesses) they bring to the fight.

Aster: The Multi-Chain Volume Juggernaut

Profile: Aster burst onto the scene in late September 2025, essentially out of nowhere, and within weeks was leading the entire perp DEX market by reported volume. In a single week, Aster’s daily trading volume rocketed from around $1B to over $70B9, an almost unbelievable growth curve. At its peak in early October, Aster claimed nearly 70% of market share by volume - a dramatic swing that temporarily knocked Hyperliquid down to a minority share. This growth coincided with the launch of Aster’s token and aggressive incentives, which we’ll cover shortly. Aster is incubated with serious backing: it emerged from a merger of a project called APX Finance with others, and is endorsed by Binance’s leadership - including public support from former CEO CZ (Changpeng Zhao). Binance’s venture arm (now YZi Labs) invested in Aster, lending it credibility and perhaps strategic advantages (like BNB Chain integration). In essence, Aster is positioned as a “Binance-adjacent” perp DEX - which immediately caught traders’ attention given Binance’s influence in crypto trading.

Architecture & Multi-Chain Strategy: Aster’s key differentiator is its multi-chain deployment. Rather than building a single appchain, Aster chose to spread across multiple popular chains to meet users where they are. As of Oct 2025, Aster runs on BNB Chain, Ethereum, Solana, and Arbitrum, with plans to even launch its own L1 (an Aster Chain using zk technology) in the future4. This multi-chain approach means users on those ecosystems can trade on Aster without bridging assets to a new chain. For example, a BSC user can trade Aster perps using BUSD/BNB liquidity directly on BSC, while an Ethereum user can use ETH/USDC on mainnet, etc. Aster essentially eliminates bridging friction for onboarding - a smart move, as bridging has historically been a UX barrier and security risk in DeFi. Each instance of Aster on different chains taps into that chain’s native liquidity and userbase. To coordinate this, Aster likely uses a centralized matching engine or cross-chain messaging for some features, but specifics are under wraps. It’s not fully clear if order books are independent per chain or shared; however, they brand themselves as a unified platform, so possibly some cross-chain aggregation happens behind the scenes. Nonetheless, being on multiple chains gave Aster a huge user acquisition boost - it could appear in the wallets/apps that millions already use on BSC or Solana, rather than asking them to come to a new chain.

Aster also offers two trading modes: “Simple mode” which is a quick swap interface backed by an ALP liquidity pool (akin to GMX’s GLP model) allowing up to 1001× leverage (!) for major pairs, and “Pro mode” which provides a full order book interface with advanced order types and MEV-resistant design. The Simple mode is aimed at casual users who want high leverage and instant execution (with the pool as counterparty), whereas Pro mode caters to sophisticated traders who want to place limit orders on a CLOB. This dual approach is clever: it merges the ease of an AMM/pool (especially useful on chains less known for order book activity) with the precision of a CLOB for those who need it. It essentially tries to capture both GMX-style users and dYdX-style users under one roof.

Product Innovation - Stocks and Hidden Orders: One of Aster’s headline features is the introduction of stock perpetuals. Aster allows trading perpetual futures on major equities like Apple (AAPL) and Tesla, with crypto collateral and up to 50× leverage[4]. This is novel - it brings traditional market exposure into DeFi, letting crypto traders speculate on stock prices 24/7. The trades are settled in crypto (e.g., USDT or a stablecoin), and presumably track stock prices via price oracles. While synthetic stock trading isn’t entirely new (Mirror Protocol, Synthetix tried versions), Aster’s high leverage and integration into a perp trading interface are pushing the envelope. It’s an attempt to attract a broader trader base and differentiate with something Hyperliquid doesn’t (yet) offer. Another innovation is Aster’s “hidden orders” feature. Traders can place limit orders that are not visible on the public order book until they start filling, to prevent market impact and front-running. This is akin to “iceberg” or hidden orders on centralized venues, and implementing it on-chain is non-trivial (likely they match these orders off-chain or via some commit-reveal scheme). It indicates Aster is thinking about the MEV and front-run problem - by offering hidden orders, they cater to larger traders who don’t want arbitrage bots jumping in front of them. Additionally, Aster supports yield-bearing collateral (e.g., you could deposit an interest-bearing version of BNB or a stablecoin LP token as margin) so that your collateral earns yield even while you trade. This is a nice user perk: it increases capital efficiency, something professional traders love.

Liquidity and Volume - The Big Question Marks: By raw numbers, Aster’s rise was staggering. It reportedly processed upwards of $70B daily volume by end of Sep 2025[9], and in September it accumulated about $420B total volume - making it the #1 DEX that month. It also boasted very high revenue on certain days: on Sep 28, Aster’s fee revenue supposedly hit $25M in 24h, dwarfing Hyperliquid’s ~$3M that day. These figures, if genuine, imply deep liquidity and active trading. However, almost every analyst has raised an eyebrow at Aster’s numbers. On-chain data suggests much of Aster’s volume was likely inorganic. One red flag: Aster’s volume/TVL ratio was over 70:1, far outside the normal range of 3-7:1 seen in other platforms. That implies an incredible amount of churn on each dollar of liquidity - a classic sign of wash trading or incentive-driven trades. Indeed, Aster’s incentive program (a points system for traders, likely tied to a future airdrop or reward) strongly encouraged users to trade frequently with themselves or bots to rack up points. This “trading rewards” program led to what appears to be massive wash trades - essentially volume for volume’s sake, to farm rewards. The result is that Aster’s reported volume may be hyper-inflated relative to genuine user-driven activity. The team behind DeFiLlama even publicly accused Aster of basically faking volume, and removed Aster from their volume tracking charts as a result. One investor quipped that Aster’s volumes “may be as close to 100% inorganic as we’ve seen on any perp DEX”, which is scathing. For Aster, the challenge ahead is proving real liquidity and retention once the rewards and airdrop farming frenzy settle down. Its open interest provides a clue: at ~$3B OI, Aster’s OI is only 1/4 of Hyperliquid’s ($13.5B), which means a lot of Aster’s volume is very short-term churn rather than long-term positions. This again hints that arbitrage bots or farmers are doing high turnover trades for points, rather than organic users taking directional bets.

Token and Economics: Aster’s token (ASTR, presumably) launched mid-September 2025 and saw a meteoric price rise - roughly 10× from ~$0.17 to ~$1.90 within days, giving it a fully diluted valuation around $14B[7]. This pump was fueled by hype (CZ’s endorsement on social media was a big factor) and the narrative that Aster could be “the next Hyperliquid.” It’s important to note that unlike Hyperliquid, Aster did have significant early investment (Binance-affiliated funds, etc.), so one assumes token allocations exist for those backers that may vest in the future. Aster’s model so far appears very incentive-driven: it’s effectively paying traders (via point rewards and possibly token emissions) to bootstrap usage. This is a tried-and-true play in crypto (liquidity mining), but it can be dangerous if the usage isn’t sticky after the rewards taper. The fact that Aster is considering launching its own L1 chain implies a longer-term plan to replicate Hyperliquid’s vertical integration (perhaps to reduce costs and have their own validators). They also launched their own stablecoin (USDA or similar) or plan to, given mention of a stablecoin and yield integrations. The breadth of their product (spot, perps, yield, a planned chain) suggests they aim to be a one-stop DeFi trading ecosystem - analogous to how Binance covers everything in CeFi. This synergy could be powerful (imagine using yield farming on BSC and instantly using those assets as collateral on Aster perps, etc.). However, it’s an execution-heavy strategy and Aster is doing a lot at once.

Outlook: Aster has certainly made a splash - possibly the only project to ever knock Hyperliquid off the top volume spot, even if artificially. Its strengths: accessibility (multi-chain, high leverage for degen traders, stock offerings, easy mode for newbies) and aggressive incentives. Its weaknesses: questionable organic volume, potential regulatory scrutiny (offering 1000× leverage and stock derivatives with no KYC is asking for a regulator’s attention[1]), and unproven durability (will users stay if/when the Aster token rewards dry up?). The big question: Is Aster a firework or a star? In other words, will it flash brilliantly thanks to incentives and then fade, or will it convert that initial momentum into a lasting community and deep liquidity? Its backers (including CZ) give it credibility and likely considerable resources. If Aster can clean up its volume to be more organic and deliver on its tech promises (especially launching its own high-performance chain to close the tech gap with Hyperliquid), it could remain a top contender. At the very least, Aster has forced Hyperliquid to respond, as we’ll discuss later.

Lighter: The Zero-Fee zk-Rollup Contender

Profile: Lighter positions itself almost as the ideological opposite of Aster. Where Aster is all about massive volume and broad reach, Lighter is focused on trust, transparency, and efficiency. Founded by former Citadel engineers and backed by a16z and other big VCs, Lighter built a custom solution using cutting-edge cryptography. It started 2025 relatively under the radar but steadily grew with a product-first approach. By mid-2025, Lighter was handling a solid $3B daily volume on average, and over $7B daily by early October while still in a closed beta. It ranked third in September with ~$164B volume, which is impressive given it wasn’t even fully public. Lighter only opened to the public on Oct 2, 2025, when it launched its mainnet to everyone. The anticipation was high, because Lighter’s unique selling propositions made it stand out.

Technology - zk-Rollup and Verifiable Fairness: Lighter’s core innovation is being built as a zero-knowledge rollup (zkRollup) on Ethereum’s Layer 2 (specifically on Arbitrum’s tech stack, though possibly a bespoke chain anchored to Ethereum)[10]. Every trade, order, cancellation, funding payment, and liquidation on Lighter is accompanied by a zero-knowledge proof that the action is valid. These proofs are aggregated and posted to L1 (or at least to an Arbitrum chain) such that the state of Lighter’s exchange can be mathematically verified at all times. The benefit? Users don’t have to trust the exchange operator - even if Lighter matches orders off-chain, the zk proofs on-chain guarantee that the matching was done correctly and funds are safe. Lighter touts this as providing “cryptographic guarantees of fairness that no other exchange can match”. In essence, while Hyperliquid asks you to trust its validators and Aster might have some opaque cross-chain matching, Lighter aims for maximum transparency and trustlessness via math. This appeals to the purists and to any trader nervous about hidden manipulation. The trade-off might be slightly higher latency (generating zkProofs can introduce delay), but Lighter’s team likely optimized it heavily. If done well, this approach could combine the best of both worlds: CEX-like speed and DeFi-like auditability.

Zero Fees - A Bold Bet: Lighter made waves by announcing a zero trading fee policy for takers (especially retail-sized traders). Most exchanges, including Hyperliquid and Aster, charge fees (usually around 5 to 10 bps per trade, sometimes less for makers). Lighter said: nope, we won’t charge you any trading fee. This is extremely attractive to high-frequency traders and anyone doing many transactions - fees can really add up. How can Lighter afford this? Likely by subsidizing with investor capital (classic growth strategy: burn money to get users) and by monetizing elsewhere (perhaps wider spreads via their liquidity providers, or future value capture like a token). For now, the zero-fee model definitely helped fuel its growth: by September, with invite-only access, Lighter was still moving $7B a day, meaning traders were very active. Free trading is a powerful incentive, essentially an indirect “rebate” to users. Lighter’s gamble is that they can achieve critical mass of volume and maybe later introduce some fees or other revenue (or launch a token that captures value differently). We’ve seen similar in CeFi (exchanges like Robinhood popularized zero commission trading by selling order flow instead). It’s possible Lighter could charge market makers or have a tiered fee where whales pay and small fish don’t. So far though, it’s been a key differentiator: Hyperliquid’s taker fee ranges ~0.02-0.05% (variable), whereas Lighter’s is 0%. One competitor even advertised that their 0.01% fee undercut Hyperliquid’s fees, but Lighter just obliterated that comparison by going to 0.

Liquidity via Community LLP: Lighter, like Hyperliquid, also employs a community liquidity pool. The Lighter Liquidity Pool (LLP) is similar in concept to Hyperliquid’s HLP - users can deposit assets to provide liquidity for the order book and earn yields. And Lighter’s yields have been eye-popping: an average of 60% APY in 2025 for LLP providers! This suggests either very lucrative trading flow (maybe internal market maker strategies capturing a lot of PnL from flow) or heavy token incentives paid to LPs (perhaps Lighter’s investors subsidizing yield). Either way, a 60% return drew plenty of deposits, giving Lighter a liquidity backbone to tighten its spreads. The team has plans to further integrate the LLP with trading - e.g. allowing LLP depositors to also use their LP tokens as margin for trading, effectively letting users “trade and earn yield on the same capital”. That’s a step beyond others in terms of capital efficiency, and it highlights Lighter’s ethos of maximizing user benefit.

Backing and Team: Lighter’s founders being ex-tradfi (Citadel) gives it credence in understanding how pro trading systems work. Its backers like Andreessen Horowitz (a16z) give it deep pockets for the zero-fee war. It reportedly has other big-name investors, which means when it comes time to launch a token, there will be expectations - but also resources to bootstrap a large ecosystem. Lighter hasn’t launched a token yet (as of Oct 8, 2025), which could be strategic: build usage first, then drop a token to reward users (similar to Hyperliquid’s delayed airdrop approach). That could ignite another wave of volume if people start farming a potential Lighter airdrop.

Volumes & Performance: Lighter’s performance metrics prior to full public launch were strong. ~$7B daily volume invite-only implies significant demand. When it opened on Oct 2, some expect its volumes to climb further as more users onboard. It’s still behind Hyperliquid in open interest and total liquidity - likely because being invite-only limited big whales or widespread adoption. But it also hasn’t shown any large-scale issues or exploits, which is a good sign for its tech. It might have slightly fewer markets than Hyperliquid (to start), focusing on top crypto perps first. One interesting stat: by September, Lighter had 188,000 registered accounts and ~50,000 daily active users even in beta8, showing a healthy user base ready to ramp up.

Risks & Sustainability: The obvious question on Lighter is sustainability of zero fees. While great for growth, at some point the business needs revenue. Lighter could plan to introduce fees later, or rely on a token that accrues value from something like a fee switch. Alternatively, they might charge large traders or monetize order flow (though on a DEX that’s tricky). Another risk is complexity - the zk-rollup design is cutting-edge, which sometimes can hide new failure modes or simply slow down iteration. If any bug in the prover or circuits was found, it could compromise the exchange or force downtime (though audits and formal methods likely were done). So far no incidents reported, which is a testament to the tech. There’s also the Regulatory angle: Lighter’s approach (unlike Aster’s wild leverage) is relatively conservative - it doesn’t boast 1000× leverage or stocks, it’s more about crypto perps with fairness. Still, as with any derivatives platform without KYC, it could face future pressure or geoblocking requirements. But among the competitors, Lighter seems to be playing the longer game of “credible neutrality” and sound tech, which could earn it favor if regulators differentiate more responsible players.

Summary: Lighter is the “slow and steady” challenger, but with some flashy moves (zero fees). It appeals to a segment of traders that values fairness (no MEV, no hidden manipulation) and low costs, perhaps even at the expense of not having every bell and whistle. Its strengths: cryptographic integrity, no fees, high yield (which attract volume and liquidity organically), and serious backing. Its weaknesses: still building out feature parity (e.g., fewer markets than Hyperliquid yet), and the fact that until a token is out, it’s burning cash for those free trades. If Hyperliquid is the incumbent giant and Aster is the brash volume hacker, Lighter is the precision engineer - focusing on building a better machine and trusting that users will come for the quality. The coming months will show whether that strategy can carve out equal market share or if it will remain a strong but secondary player.

Other Notable Challengers

Beyond the “big three,” the perp DEX space has a constellation of other projects. It’s worth briefly noting a few:

edgeX: An Arbitrum-based high-performance perp DEX that often ranks in the top 5 by volume (recently ~$4-5B daily). edgeX presents itself as an “orderbook-based DEX with native CEX-like experience”. It ran a points campaign (“Open Season”) similar to others, and is rumored to be evolving into its own app-specific chain. edgeX’s strategy seems to mirror Hyperliquid’s (speed on Arbitrum now, perhaps own chain later). It’s a contender to watch, though currently behind Lighter in usage.

Bulk: Mentioned earlier, Bulk is a newer entrant that attracted VC funding (Robot Ventures and others co-led an $8M seed). Bulk’s CEO openly aims to capture institutional flow and even made the bold claim that whoever wins could hit a trillion-dollar valuation. Bulk’s product details are scant, but it likely focuses on some specific niche or integration to differentiate (perhaps institutional connectors or a unique risk system). It’s in early days.

Drift (v2): On Solana, Drift is trying to stage a comeback (after Mango’s fall) by offering a robust perp DEX with features like subaccounts and a partial backstop mechanism. Solana’s tech (high throughput, low latency) gives Drift an inherent advantage, but the Solana DeFi ecosystem isn’t as vibrant as EVM’s at the moment. Drift’s OI is modest (under $500M)2.

Pacifica, Zeta: These names surfaced in Arca’s analysis as new players with “variant strategies”1. For instance, Pacifica might be exploring hybrid orderbook/AMM designs or new asset classes, while Zeta could refer to ZetaChain’s derivative plans or another Solana-born project (there was a Zeta Markets on Solana for options; unclear if same one pivoting to perps). They’re still small but illustrate the breadth of experimentation.

Injective, Vertex, etc.: Injective Protocol operates a Cosmos-based chain and has an orderbook exchange that’s been steadily improving volumes (though still < $1B/day typically). Vertex on Arbitrum launched a hybrid perps+AMM platform that gained some traction mid-2023. While these are noteworthy, by late 2025 their market share is overshadowed by Hyperliquid, Aster, Lighter - but they often have loyal communities or unique features (e.g., Vertex integrated with spot markets and had a cross-margin with lending).

dYdX v4: Finally, we should note dYdX’s own re-entry attempt. In late 2023 and 2024, dYdX launched v4 as an independent Cosmos app-chain, fully decentralized orderbook. However, due to earlier missteps (and perhaps the Cosmos tech being new for them), adoption has been lukewarm. By 2025, dYdX’s market share is negligible1 - a dramatic fall from its past glory. It serves as a bit of a ghost of Christmas past for the new entrants: a reminder that an early lead can evaporate if you don’t adapt and if you alienate your community.

The Competitive Landscape: In summary, the perp DEX arena is crowded and fiercely competitive. But it’s not a zero-sum in the short term - the overall pie is growing so rapidly (remember, only ~10% of perp volume is on DEXs so far) that multiple platforms are seeing record volumes simultaneously. As Arca’s report framed it, this is like an arms race where different philosophies are clashing:

Hyperliquid represents max performance and scale - proving DeFi can outdo CeFi in raw power.

Aster represents accessibility and ambition - pushing boundaries with multi-chain and cross-asset offerings (even if it means turbo-charging with incentives).

Lighter stands for transparency and fairness - rebuilding trust through tech (zk) and user-friendly economics (no fees).

Each is carving a niche: Hyperliquid for pros who need speed and depth, Aster for opportunists chasing incentives or wanting extreme leverage and asset variety, Lighter for those valuing fairness and cost efficiency. It’s very possible we won’t get a single winner-take-all; instead, each could sustain a segment of the market. Traders themselves might arbitrage between them - e.g., one could use Hyperliquid as primary but switch to Aster when there’s a juicy liquidity mining campaign, or use Lighter for assets where they want fee-less hedging, etc. The competition has already hugely benefited users: fees have dropped, spreads tightened, and product innovation accelerated. The war is making everyone up their game. Hyperliquid, for instance, has hinted it may cut fees further and deploy its own “war chest” of funds to reward loyalty or liquidity in response to rivals’ moves. We are likely entering a phase of “vampire attacks” (one platform trying to lure users/liquidity from another with incentives) in on-chain perps, much like we saw in DEX wars of 2020 for spot exchanges.

In the next section, we’ll zoom into those “pop markets” that stress test these exchanges, and how each platform’s design handles (or struggles with) sudden storms - whether that’s a memecoin mania or a major token listing. Understanding this will further illuminate the differences in their risk models and depth. After that, we’ll quantify the economics (volume, fees, etc.) side-by-side and then scenario-plan the future of this war.

Pop Markets and Stress Tests: Meme Manias, New Listings, and Volatility Shocks

One of the best ways to judge a trading platform is how it handles the wild days - when a token goes parabolic or tanks overnight, when volumes spike and emotions run hot. These “pop markets” can be memecoin frenzies, major news events, or novel asset launches. They stress test liquidity depth, matching engines, and risk management. The perp DEX war has already seen several such episodes, offering a glimpse into each platform’s resilience and design philosophy.

Meme Coin Frenzy - Hyperliquid’s PUMP and Whale Woes

2025 had its share of memecoin crazes - and one of the most dramatic played out on Hyperliquid with a token aptly named PUMP. PUMP was a meme coin that started gaining traction (outside of Hyperliquid) due to viral social media hype and aggressive buyback/burn gimmicks by its issuers. Hyperliquid listed PUMP-PERP relatively early, providing a venue for traders to long or short this volatile coin with leverage. In August-September 2025, PUMP’s price skyrocketed over +150% in a short span, reaching a multi-billion dollar market cap out of nowhere. Many traders made fortunes; others got wrecked. On Hyperliquid, an anonymous whale (account “btc@tuta.com”) took an especially audacious bet: he amassed an 85.6 billion PUMP token short position at 5× leverage. In nominal terms, this short was worth about $64 million at entry - indicating enormous size. As PUMP’s price kept climbing (fueled by frenzied retail buying and maybe manipulation), this whale’s position went deeply underwater. At one point in late September, he was facing an unrealized loss of $35 million on the PUMP short alone, plus additional losses on other shorts (SOL, LINK) pushing total unrealized loss to ~$44M.

This was a pivotal stress test for Hyperliquid. A position that size, normally, could threaten the exchange: if the trader got liquidated into an illiquid upward market, it might not find enough buyers to cover, potentially blowing through insurance funds or causing a cascade. Hyperliquid’s order books were deep, but PUMP’s meteoric rise meant liquidity on the short side was thinning. According to analysis, Hyperliquid avoided immediate liquidation of this whale due to his collateral and perhaps adjusted margin requirements, but the situation was dire enough to draw public scrutiny. Eventually, PUMP’s rally cooled (likely in part because traders saw how one big short was “trapped,” and once his position stabilized, some mania died down). The whale remained solvent, even having earned ~$1.44M in funding fees on the short during the ordeal (since shorts were paying longs while price was above index, he was receiving funding). Remarkably, this account was historically profitable ($9.5M net profit before this episode), suggesting it might be an arbitrage or sophisticated trader rather than a clueless ape.

From this PUMP saga, a few things stand out:

Hyperliquid’s Depth and Risk Controls: The fact that an $85B-token short (tens of millions USD) could be opened on Hyperliquid indicates massive available liquidity and high position limits. Hyperliquid allowed up to 40× leverage, but effectively for something like PUMP the margin requirement likely dynamically increased as the position grew (to avoid instant blowouts). Hyperliquid’s earlier enhancements - dynamic risk margins and anti-manipulation rules - were specifically cited as mitigating factors that helped contain this situation. For example, if the order book started thinning, the required margin may have increased, forcing the trader to add collateral or reduce position before catastrophe. Also, Hyperliquid likely throttled the speed of liquidation to prevent a sudden dump (partial liquidation over time vs everything at once). The incident shows that Hyperliquid can weather very large trades on highly volatile assets, but it also underscored the need for vigilance. They emerged without an exchange-wide issue, which is commendable. The PUMP short became almost a meme itself on CT (crypto Twitter) - people were tracking it, joking about “when will he get liquidated?” - and Hyperliquid got a lot of attention from it. Some saw it as proof that on-chain transparency is a double-edged sword: everyone can see the whale’s position and pain (which could invite targeted squeezes), but also it forces the platform to be on its toes. Hyperliquid passed this test by adjusting margins and relying on its liquidity providers to stabilize the market. Notably, Hyperliquid had a precedent with another token (XPL) that caused issues, after which they implemented stress alerts to detect such scenarios early.

Funding Rates and Mechanics: This scenario is a textbook case of how funding rates work in perpetual swaps. Because PUMP’s perp price was likely above the true spot (due to longs piling in), funding was probably heavily positive, meaning shorts like the whale received payments regularly from longs. The whale earned $1.44M in funding over time1, which partially offset his losses. A quick formula: funding payment = position size × funding rate. If his position was $64M notional and, say, PUMP’s hourly funding was 0.01% (just a guess in such a hot market), he’d get $6,400 per hour. Over weeks, that adds up. This dynamic is crucial: it incentivizes arbitrageurs to short when price is too high above fair, but in PUMP’s case, no arb could easily bring price down due to the mania. The high funding payout kept the whale from being liquidated sooner (because he was effectively paid to stay short), but if price kept rising, that wouldn’t save him. The equation can be exemplified: if PUMP perp is 5% over spot, and funding is paid every 8 hours, a short might receive ~0.625% of position per day (assuming 5% annualized to per 8h, for simplicity). On $64M, 0.625% daily is $400k/day - huge, but PUMP was moving ±20% in a day, so it’s not enough alone. Our whale survived because he had deep pockets and added margin or because price eventually reversed in time.

Implications for DEX Design: The PUMP case prompted questions: Should DEXes allow any one account to accumulate such a giant position on a low-cap memecoin? Hyperliquid did impose some limits (and maybe this was within their limits). Traditional risk management might cap exposure or require higher margin for such “isolated” assets. Hyperliquid likely revisited these parameters. But the flip side is, if they restrict too much, they lose the volume and appeal for whales. It’s a balancing act. Also, on a DEX, you can’t selectively force someone out unless through the protocol rules; everything is transparent and mechanical. In CeFi, sometimes risk teams manually intervene - not possible (easily) in DeFi. Hyperliquid’s solution is to bake those policies into code (auto-increase margin requirements, etc.) and broadcast warnings (stress alerts) to all users, which they reportedly do1.

New Token Listings - Price Discovery on DEX First

Another type of “pop market” scenario is when a new token listing draws speculators in droves. Hyperliquid notably offered pre-listing futures for the Plasma (XPL) token - a token associated with Tether’s Plasma network - before that token was officially live. Essentially, Hyperliquid created a perpetual futures market for XPL based on expectation of its future value, and traders started pricing it days or weeks in advance. The result: XPL pre-market on Hyperliquid traded up to ~$0.70, then when real spot markets opened and hype kicked in, it soared to $1.40. This indicates that Hyperliquid served as a price discovery venue even ahead of centralized exchanges or official markets. That’s a powerful role - being the first market where price is set. It attracts a lot of volume from those wanting early exposure. It’s also risky: without an underlying, it’s basically trading on sentiment and whatever reference the exchange sets (maybe an index of IOUs or so). Hyperliquid pulled it off, showcasing that their infrastructure and liquidity can handle even completely new assets. It’s akin to offering an IPO futures contract. For traders, this is exciting - you don’t have to wait for Binance or Coinbase to list, you can trade on Hyperliquid ASAP.

Aster similarly tries to list trending tokens quickly (one reason they wanted multi-chain is to list new BSC or Solana ecosystem tokens natively). However, Aster’s more notable listing hype was its own token launch. When Aster’s token went live on Sept 17, it became a “pop market” in itself, surging 10× in days4. Aster perps likely were highly traded during that time, as traders speculated on its value with leverage (if Aster had ASTR-PERP from day one, which it likely did). The irony of a perp DEX offering perps on its own token can be wild - because huge activity in the token translates to both trading volume and platform revenue (if organic). Indeed, when Aster’s token pumped, so did its platform’s usage in a reflexive loop.

Cross-Asset Volatility (Stocks, etc.)

Aster’s introduction of stock perps adds another dimension to volatility scenarios. For example, if Apple had an earnings surprise and its stock moved 10% after hours, Aster’s AAPL-PERP would react immediately (trading 24/7), whereas traditional markets are closed. This could cause huge volume and volatility on Aster if, say, crypto traders try to front-run the next day’s NASDAQ open. It’s an open question how Aster handles the oracle pricing and settlement for these stock perps. If the oracle is reliable (maybe from a regulated CFD provider or something), it could work, but any delay or manipulation could be problematic. It hasn’t been tested by a major event yet, but one can imagine a scenario: e.g., Tesla’s stock jumps 20% on some news at a time U.S. markets shut - Aster’s TSLA-PERP would gap up; anyone short might get liquidated quickly. Does Aster have circuit breakers for such scenarios? Traditional exchanges often halt trading on too much gap; DEXs typically don’t, except if oracle fails. So these cross-market products could present new kinds of stress tests. We haven’t seen a big one yet, but the potential is there.

Latency and MEV in Fast Markets

During volatile events, the latency of each platform is challenged. Hyperliquid’s sub-second finality generally ensures even in rapid moves, orders execute near-instantly. Lighter’s zk-rollup might have a slight lag (depending on how often proofs post - possibly every few seconds or faster). Aster’s multi-chain approach might suffer if one chain (like Ethereum L1) is congested right when volatility hits. For instance, if an Ethereum-based user on Aster tries to adjust a position during a gas spike, they could be slowed. Meanwhile, a BSC user might be fine. This uneven latency could be arbitraged by savvy players (they’d prefer the fastest chain environment to trade). It’s a complexity Aster will face: maintaining a synchronized experience across chains. Also, MEV (Miner Extractable Value) comes into play. Hyperliquid, by having its own chain, can minimize MEV - there’s no external miner, and presumably Hyperliquid’s validator set can’t front-run because order matching is internal (and maybe fair-ordering is enforced). Lighter explicitly touts MEV protection as a feature (and hidden orders help with that)1. In contrast, a multi-chain DEX like Aster might be vulnerable to MEV on each underlying chain (e.g., Arbitrum’s sequencer could theoretically re-order, or BSC validators could). If someone places a huge order on Aster’s BSC instance, a BSC validator might see it and try to profit. Aster’s hidden orders partially mitigate orderbook sniffing, but not fully if someone market orders. So during frenzies, Aster traders might suffer more slippage from arbitrage bots than Hyperliquid or Lighter traders would. That’s a nuance traders will start to notice. It ties back to technical design: Hyperliquid and Lighter chose to control the environment to limit MEV and latency; Aster chose reach at the cost of relying on varied environments.

Liquidation Cascades and Circuit Breakers

A final point on stress: do these exchanges have “circuit breakers” or pause mechanisms in extreme moves? In CeFi, exchanges sometimes halt trading if price moves too fast. In DeFi, typically not - price moves until liquidity is out. However, some DEXs can pause markets if oracle price deviates wildly or in a detected manipulation. Hyperliquid’s “systemic stress alerts” might allow devs or governance to pause a market if needed (not sure if they’ve ever used it). If a flash crash happened (say BTC flash crashes 20% in a minute due to some oracle glitch or large market sell), how each DEX handles it will matter. Insurance funds might get tapped. We know by Sept 2025, DeFi insurance funds have grown - Hyperliquid likely has a sizable safety fund from its fees, Aster presumably started one (especially as it claimed huge fee days). Lighter, with no fees, might rely on the LLP and equity capital as a backstop. So ironically, the one not charging fees (Lighter) might have less buffer to cover a sudden market mess unless they’ve provisioned one from investor funds.

So far, none of the top three have had a fatal meltdown in a volatile event - which speaks well of them. But the war is young, and as volumes scale, we’re likely to see even crazier days (imagine when crypto market inevitably hits a bull frenzy - these DEX volumes could triple, and volatility with it).

In summary, the “pop markets” have shown:

Hyperliquid’s matching engine and depth are extremely robust (handling pre-launch price discovery and giant meme trades), though it’s had to continuously refine its risk management to avoid exchange-threatening positions. It essentially functions like a top-tier CEX in these moments, with comparable or better outcomes.

Aster can accumulate insane volume on hype tokens (including its own), but questions about organic liquidity mean we haven’t truly seen how it holds up if the wash trading bots disappear. Aster’s architecture hasn’t faced a giant stress publicly beyond just sheer volume - something like a chain outage on one of its chains, or a huge gap event on a stock, will be telling.

Lighter hasn’t been battle-tested by a catastrophic event yet, but its design choices (like fairness and no fees) might actually shine during volatility - traders won’t be fighting fee costs, and zk proofs ensure no funny business. One potential issue: if network congestion on Ethereum/Arbitrum happens at the same time as a big market move, could proving or posting state lag? Possibly, but likely minor given Lighter’s off-chain proofs and use of L2.

Overall, each challenge so far has generally strengthened these platforms (Hyperliquid especially learned and adapted from XPL and PUMP incidents). These DEXs are proving that decentralized infrastructure can handle the worst the market throws, often as well as or better than centralized platforms that have human intervention (and human error).

Next, we’ll quantify the current state of the war in terms of numbers - volumes, open interest, fees, and revenue for each major platform - to get a clear picture of the scoreboard as of Oct 8, 2025. Then we’ll delve into the token-economic math that underpins their business models, before moving on to future scenarios.

Numbers and Economics: Volumes, OI, Fees, and Token Math (Oct 2025 Snapshot)

To truly grasp who’s winning (or spending) in the perp DEX wars, let’s examine the key metrics side by side. We’ll look at 24-hour, 7-day, and 30-day trading volumes, the open interest, and protocol revenues/fees for the major players as of the snapshot date (Oct 8, 2025). This will be followed by an analysis of token economics - how each platform’s token captures (or doesn’t capture) the value from those fees and what that implies for sustainability. Strap in for some numbers:

Trading Volume & Market Share

Hyperliquid: Despite new competition, Hyperliquid remains a volume beast. Over the last 30 days, Hyperliquid processed roughly $280-300 billion in perp volume. On an average day in early October, it’s doing about $10-13 billion volume, which is roughly 25-30% of all DEX perp volume on honest accounting (excluding Aster’s questionable volume). Over 7 days, that’s on the order of $70+ billion. Notably, Hyperliquid’s volume dipped in September (with ~$282.5B, down from $398B in August) as some flow went to Aster, but by early October as Aster’s wash trades cooled, Hyperliquid’s share was recovering. Realistically, if we exclude suspected inorganic trading, Hyperliquid likely still commands the largest organic user base and volumes.

Aster: Officially, Aster posted the highest volumes in late Sept: ~$420 billion in September9, averaging $14B/day, and spiking to $70B on peak days. At one point Aster claimed ~70% market share by volume. However, after adjusting for wash trading, those numbers are less impressive. DefiLlama outright stopped tracking Aster due to data manipulation allegations, which makes direct stats tricky. That said, on Oct 8, 2025, if one looked at public APIs or other trackers, you might see Aster still logging tens of billions in daily volume, but one must take it with a grain of salt. The true user-driven volume could be a fraction. Still, even a fraction (say 10-20%) of their reported $70B is significant (like $7-14B/day). Let’s assume optimistically that Aster has ~$10B/day genuine volume now - that would put it roughly neck-and-neck with Hyperliquid. Time will tell if they sustain or drop off after incentives.

Lighter: Lighter in early Oct was around $7-10B/day as it left invite-only status. This was good for roughly 15-20% of the total DEX perp volume at that time (excluding Aster’s fake). In September, it did about $164B (official) which is ~$5.5B/day average, but that was invite-only and before their public launch. We might expect Lighter’s volume to be trending up now that it’s open. It’s feasible Lighter could catch up to Hyperliquid’s daily volumes if its zero-fee model pulls enough traders.

Others: edgeX was noted at around $4.8B/day (ranking #3 or #4), and ApeX (from Bybit) around $3B. These are far behind the top 3, but not trivial. For instance, ApeX on Polygon/Arbitrum sees use by some Bybit users bridging over. GMX and dYdX by this time likely have <$1B daily each (GMX had around $500M on good days historically; dYdX v4 unknown but likely small).

In aggregate, in early October, total perp DEX daily volume (ex-Aster) was roughly $40-50B. With Aster’s reported, it was over $100B some days. The trend is clearly rising: September total was $1.05T, on track to perhaps $1.2T+ in October if trends continue.

Market share (approx, organic): Hyperliquid ~30-35%, Lighter ~15-20%, edgeX ~10%, others ~5%, and Aster perhaps ~30% if counting some real volume, else less. Essentially, Hyperliquid is still a leader but no longer the undisputed one - Lighter and Aster have carved out significant slices.

Open Interest (OI)

Open interest is a great gauge of engaged capital - how much value is locked in active positions. As noted:

Hyperliquid: OI about $12-13.5 billion. This is huge; by far the largest. It indicates many traders keep positions open there (likely due to trust in its stability, as well as perhaps lower funding rates because of deeper liquidity). High OI also contributes to Hyperliquid’s fee generation (overnight positions keep paying funding and trading occasionally to rebalance).

Aster: OI around $3 billion (according to early Oct estimates)[2]. That is significantly lower than Hyperliquid’s, reinforcing that Aster’s volume was high turnover. A healthy ratio of OI to daily volume might be, say, 1:1 or 1:2 for organic trading, but Aster was like 1:20+. If Aster’s OI grows over time while volume normalizes, that would be a positive sign (meaning real traders holding positions).

Lighter: Not explicitly reported, but if we use clues: Lighter had $7B daily volume with likely shorter-term trading (some arbitrage perhaps). It might have an OI of maybe $1-2 billion (pure guess). It wasn’t listed in the top OI protocols (DefiLlama’s top were HL $12B, then Jupiter $0.8B, etc., no mention of Lighter, possibly because it wasn’t indexed yet or because it was still beta)2. Let’s assume Lighter’s OI is still sub-billion until more traders move long-term positions there.

Others: For context, the second highest OI after HL was an exchange called Jupiter with ~$800M - likely a smaller perp platform (maybe related to Solana). Others like Drift, etc., were in the hundreds of millions. So Hyperliquid has more OI than the next 5-10 exchanges combined. That is a critical point: it shows big money trusts Hyperliquid to hold their positions (like large hedges or directional bets), whereas others have more transient use.

Fees and Revenue

Now, volume is vanity, fees are sanity. Let’s see how much users are paying and how much protocols are earning:

Fee Rate Differences: Hyperliquid charges a variable fee (it can range ~0.02% to 0.05% per trade for takers, with makers possibly lower or rebate if using HLP maybe). Aster’s fee structure isn’t public, but given one day $36B vol yielded $10M revenue11, that implies ~0.028% effective fee (which sounds like a taker fee). So Aster might be charging ~0.03% and maybe rebating some via points. Lighter currently charges 0 for most trades (so its fee revenue is near 0, aside from maybe a small spread or if any specific fees for large size/trades).

Hyperliquid Fees/Revenue: In the last 30 days, Hyperliquid collected around $95 million in fees. That’s about $3.2M/day average. The trailing 7d was $25M, and 24h around $5M on a high day. These numbers align with the idea that Hyperliquid’s annualized fee run-rate is now around $1 billion+. Importantly, Hyperliquid’s protocol revenue (the portion of fees that accrues to the protocol) is nearly the same as fees, because Hyperliquid doesn’t have liquidity mining emissions or external LP incentives to pay out. It does share some with HLP providers as yield (6-8% APY on $500M is about $30-40M/year, which is small relative to $800M revenue, and likely considered a business expense). DefiLlama data shows Hyperliquid’s annualized revenue at ~$1.08B, with protocol revenue near that since incentives are low. So effectively, most of Hyperliquid’s fees become protocol revenue (used for buybacks).

Aster Fees/Revenue: Aster had that notable stat: $10M in 24h revenue on one day in late Sep11, ranking behind only Tether in the entire crypto space for that day. Across September, if we use The Block’s data: Aster’s $420B vol and if fee ~0.03%, yields about $126M in fees for Sept. However, net revenue is likely much lower because Aster likely spent a lot on incentives (points). If many traders expect an airdrop or reward for volume, that effectively is an “expense” in token terms. We don’t have an exact number, but one clue: on Sep 28, $25M fees vs HL’s $3.2M. It’s ironic that Aster “earned” 8× fees of Hyperliquid that day, yet Hyperliquid might have much higher real revenue retention. Also, if Aster’s volumes fall after incentives, that fee peak might not sustain. We also should note: if Aster is on multiple chains, part of fees might go to market makers or as rebates. They also launched a stablecoin possibly, and have an ALP pool - it’s unclear how much of fees are distributed to LPs vs kept. If we treat them like a normal exchange, perhaps they keep most and will distribute via token (maybe buy/burn like HL or as dividends). But at this point, Aster’s sustainable revenue is very much in question. DeFiLlama’s decision to delist implies they think much of those fees are not “real” or will vanish post-rewards.

Lighter Fees/Revenue: With zero fees for most users, Lighter’s fee revenue is close to nil. It might charge a small fee to very large takers or certain advanced features, but likely negligible. Instead, Lighter “revenue” might come from spread. If Lighter’s LP (LLP) is effectively the counterparty, sometimes the LP will gain when traders lose (like GMX model). A 60% APY to LP suggests traders on average lost money (or external incentives were paid). If it’s traders losing, that means the protocol (via LP) earned from those losses. This is more like trading revenue than fee revenue. It’s hard to quantify without internal stats, but 60% on maybe $100M in LP (just guess) implies $60M/year coming from somewhere - likely trader losses or funding. If Lighter doesn’t have a token, it isn’t paying token emissions, so that yield is presumably organic PnL from market making. That indicates Lighter’s model has a built-in revenue if traders are net negative (like a casino). However, that can’t be counted on if traders as a whole break even. In summary, Lighter currently prioritizes growth over fee revenue. When it introduces a token, likely the plan is to flip on a fee (maybe a small one) or capture value through token demand for utility (like staking to get trading rebates, etc.).

Comparative Unit Economics: One interesting angle: fee per $ of volume. Hyperliquid’s effective fee is roughly 0.03%. Aster’s reported was similar (~0.02-0.03%). Lighter’s is effectively 0%. So: - Hyperliquid: Every $1B volume yields ~$300k fees. - Aster: If same fee, $1B volume ~$300k, but if much is wash, actual fees paid by distinct users might be lower (some could be rebates). - Lighter: $1B volume yields $0 in direct fees. But if LLP PnL is considered, and if say half of traders lose 0.1%, that could be $1M profit to LP on $1B (just hypothetical).

Token Value and P/E ratios: Let’s talk token economics and valuation. Hyperliquid’s HYPE token at $49.5B FDV, with $1B annual revenue, gives a Price/Sales (P/S) around 49x, and since most revenue goes to buybacks (i.e. effectively to holders), one could say Price/Earnings ~49x as well (or a bit higher if not 100% of revenue is distributed). That might seem high relative to traditional equities, but for a growth crypto protocol with 100%+ YoY growth, not insane. By contrast, Uniswap (for spot trading) had a much higher multiple relative to fees (some analysis said HYPE’s fee multiple is ~7× Uniswap’s, meaning HYPE is valued richer, which could reflect higher growth or better tokenomics)4. For Aster, FDV $14B and if it could sustain, say, $300M/year real revenue (very uncertain), that’s a P/S ~46x, similar ballpark. But if revenue collapses post-incentives, that P/S becomes meaningless. Aster’s token price will hinge on whether people believe it can maintain volumes organically. Lighter has no token yet - but one can imagine if it launched and quickly got a high FDV due to hype around zk and growth. The difference is Lighter would start at near-zero revenue. Investors might value it on user metrics instead (like number of traders, or volume growth).